Turning ₹50 lakhs into ₹5 crore may seem ambitious. However, with disciplined investing, patience, and the right strategy, it becomes achievable over time. A PMS wealth creation journey focuses on long-term compounding and high-conviction investing.

In this article, we explain how this transformation can realistically happen.

The Power of Compounding

At the core of this journey lies compounding—earning returns on accumulated returns over multiple years.

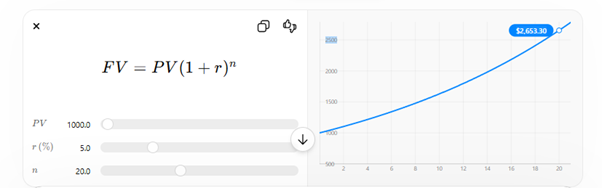

The relationship can be understood using the future value formula:

Where:

- FV = Future Value (₹5 crore)

- PV = Present Value (₹50 lakhs)

- r = annual return

- n = number of years

Time Required to Grow 10x

- At 12% return: approximately 21–22 years

- At 15% return: approximately 16–17 years

- At 18% return: approximately 13–14 years

Therefore, consistency matters more than timing the market.

What Makes PMS Different

Unlike mutual funds, PMS offers a more focused approach. In addition, it allows investors to build a customized portfolio.

Key advantages include:

- Direct stock ownership

- Personalized portfolio strategy

- High-conviction investments

- Active management

Moreover, PMS is regulated by SEBI and requires a minimum investment of ₹50 lakhs.

Phases of the Investment Journey

Phase 1: Foundation (Years 1–3)

Initially, the focus remains on stability and steady growth.

- Strategy: Large-cap and quality mid-cap stocks

- Expected returns: 10–14%

At this stage, investors must stay patient and avoid reacting to short-term volatility.

Phase 2: Acceleration (Years 4–10)

As time progresses, compounding begins to accelerate growth.

- Strategy: Increased exposure to mid-caps and growth sectors

- Expected returns: 14–18%

Additionally, earnings growth and sector rotation play a key role here.

Phase 3: Wealth Multiplication (Years 10+)

Eventually, exponential growth starts to appear.

- Strategy: High-conviction bets and long-term winners

- Expected returns: 15–20%

In fact, most wealth gets created in this phase.

Sample Growth Projection

| Year | Portfolio Value (15% CAGR) |

|---|---|

| 0 | ₹50,00,000 |

| 5 | ₹1.01 crore |

| 10 | ₹2.03 crore |

| 15 | ₹4.08 crore |

| 17 | ₹5+ crore |

Clearly, growth starts slowly. However, it accelerates significantly over time.

Strategy Behind This Growth

1. Concentrated Portfolio

Typically, portfolios include 15–25 stocks. As a result, the focus remains on quality over quantity.

2. Long-Term Holding Approach

Investors hold strong businesses for years. Consequently, they avoid unnecessary trading.

3. Sectoral Opportunities

Investments focus on long-term themes such as:

- Manufacturing

- Financial services

- Capital goods

- Renewable energy

Risks and Reality Check

Despite the potential, this journey is not linear.

Key risks include:

- Market corrections

- Short-term underperformance

- Stock selection errors

At times, portfolios may decline by 20–30%. Nevertheless, disciplined investors stay invested.

Taxation Impact

Unlike mutual funds, PMS taxation works differently.

- Gains are taxed in the investor’s hands

- Both short-term and long-term taxes apply

- Higher turnover can increase tax liability

Therefore, efficient portfolio management becomes crucial.

Who Should Consider This

This strategy suits:

- Investors with ₹50 lakhs or more

- Long-term investors (10–15+ years)

- Individuals comfortable with volatility

However, it may not suit short-term traders or conservative investors.

Conclusion

A PMS wealth creation journey requires patience, discipline, and a long-term mindset. While markets fluctuate in the short term, consistent investing and compounding drive long-term success.

Ultimately, wealth creation is not about speed. Instead, it is about staying invested long enough for compounding to work.

Total Users : 11424

Total Users : 11424